3 Ways AI is Transforming Property Insurance

Wondering about the impact of artificial intelligence (AI) in property insurance? In this post, we look at three ways AI is transforming insurance throughout the insurance value chain.

Key Takeaways

- Thanks to digital-first brands like Amazon and Netflix, AI-enabled personalization is expected for every business—including P&C insurers

- Geospatial analytics, computer vision, and other forms of AI are increasingly used to quickly and accurately assess and price risk for truly fitted cover

- IoT-enabled smart home technologies paired with AI-driven claims processes can help carriers shift from reactive claims handling to proactive loss prevention.

- By 2030, over 50% of routine property claims may be automatically processed and paid using AI

- Today, 90% of insurance executives identify AI as a top strategic initiative for their organizations, and 70% of insurers had implemented AI in at least one business function as of April 2025.

Artificial Intelligence (AI) in Insurance

Artificial intelligence or AI is the ability for computers to do tasks and solve problems that would otherwise require human intelligence, faster and more efficiently. In the insurance industry, AI is applied to accelerate processes and make use of an ever-expanding universe of data to offer personalized, proactive coverage.

In an April 2025 survey, 90% of insurance executives reported seeing AI as a top strategic initiative for their organizations. Indeed, the value of AI in the global insurance market is expected to reach nearly $80 billion by 2032, up from just $10 billion this year. Much of this is driven by consumer adoption of digital channels for buying and managing insurance, which in turn has propelled P&C insurers to quickly digitize more of their operations. For digital-savvy insurance customers, the benchmark for success is no longer just other insurers. It’s Amazon, Google, and Netflix. Digital convenience? That’s just expected. Fast, friendly service? What else is new? As Insurance-Edge.com puts it, with $170 billion in premiums at stake, AI’s ability to expedite and enhance processes throughout the insurance value chain is a proposition insurers can’t afford to get wrong. Let’s take a closer look at three of the most transformative impacts AI is having on P&C insurance today.

Underwriting Gets Personalized With AI

Thanks to popular, digital-first brands, consumers want companies to reach out to them with recommendations based on their unique needs and make it effortlessly easy to act on them. Perhaps most of all, they prize tech-forward brands that can prevent or mitigate issues before they become costly problems. Today, AI is used to mine core systems and external data sources to profile existing and prospective customers in order to help both personal and commercial lines underwriters understand risk and accurately offer and price highly personalized content, products, and services.

Generative AI, for instance, can help facilitate instant, personalized support and quoting via AI-driven chatbots and virtual assistants. These models analyze customer data to offer tailored recommendations and to quickly generate the necessary forms to quote and bind service 24×7. When applied to customer interactions, policy generation, and predictive analytics workflows, Bain & Company predicts that GenAI can help an insurer increase revenues by 15% to 20% and reduce costs by 5% to 15%. Indeed, just as Amazon might suggest a new product of interest based on your profile or purchase history, generative AI-based tools enable insurers to send messages, for instance, to a customer or prospect about new home coverage products where her children reach prime trampoline age, or car policy details when they’re approaching their 16th birthday.

With new forms of agentic AI capable of performing asks autonomously, they can automate this at scale, across the carrier’s entire book of business. These same technologies can also help transform commercial lines underwriting by performing initial risk assessment and automating pre-clearance checks to dramatically reduce manual workloads and accelerate aggregate decision making. As FinTech Global reports, 50% of insurers plan to adopt agentic AI this year.

Reassessing Risk

AI is also crucial to quickly and accurately price coverage based on the associated risk and needs of the customers. This is essential for customers shopping for insurance online and for whom the first to respond with a good rate usually wins. It’s also business-critical to the insurer. Today’s cloud-connected insurance platforms make use of a wide range of data that is analyzed using AI to score risk and personalize cover in mere moments.

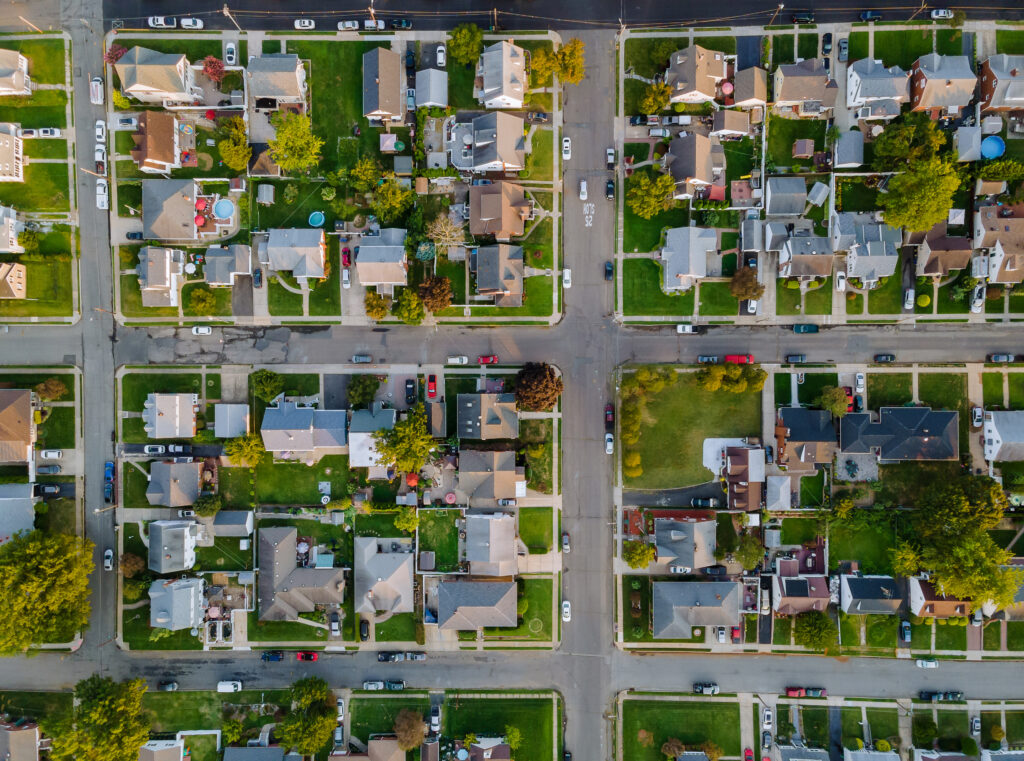

In homeowner’s insurance, for instance, this can include crime statistics, past repair permits, previous claims, and more. It also includes geospatial property analytics that use high-res aerial photography, computer vision, and other forms of AI to instantly provide an accurate, up-to-date assessment of roof condition, fire risk, the presence of a backyard pool, or debris, or hundreds of other factors impacting risk and valuation.

Our own solution, for instance, includes a Roof Condition Rating (RCR) that analyzes hundreds of different data points to provide an accurate assessment of roof condition. This can reduce the need for an inspection and the likelihood that the premium will need to be adjusted after the policy is already bound. (In habitational and small commercial lines, this and other forms of commercial property intelligence assess loss-predictive property characteristics to achieve better COPE assessments, smarter underwriting decisions and to accurately match rate to risk.)

Meanwhile, mobile apps like HomeZada enable customers or inspectors to scan the interior of their homes using their smartphone’s camera, leveraging AI to assess condition and document belongings, cross-referencing them with replacement costs to accurately price a policy. Meanwhile, property intelligence offerings like our Living Area solution deliver the AI-based, multi-source approach needed to accurately calculate Coverage A, assess risk, and set premiums. Even small inaccuracies there, at scale, can have enormous consequences on exposure at a time when two in every three homes is underinsured by an average of 22% and as high as 60% or more. Our own researchers have found this one factor alone represents a $2 billion opportunity for carriers—just from making corrections to most severely underestimated living area values in their portfolios.

Reinventing Operating Models

An expanding world of smart home sensors and other Internet of Things (IoT) devices mean AI is quickly enabling proactive coverage that alerts the insurer and the homeowner to a break in, or fire, or a leak is detected in an upstairs bathroom. Put simply, AI is enabling insurers to move to more proactive and preventative operating models that deliver added value and save both the policyholder and insurer potentially large sums of money. Devices that monitor for water leaks, for instance, could cut leak-related insurance losses up to 90% this year.

Likewise, property condition intelligence can be used to lower rates for homeowners who take steps to mitigate wildfire risk by clearing brush and other vegetation away from their home or address other perils that could lead to costly claims.

Claims: AI at the Moment of Truth

When it comes to insurance, a claim is the ultimate moment of truth. Today’s policyholder expects a fast, frictionless, and transparent claims experience. Whether it’s through IoT or machine learning and other forms of AI, insurers are embracing technologies that enable them to proactively engage policyholders and optimize claims workflows to improve efficiency and enhance customer satisfaction.

Among other things, AI can automatically extract information from property damage reports, repair estimates, and other documents, reducing manual data entry and errors and freeing adjuster to provide a more concierge level of service. Ai can also prioritize claims by severity and urgency, ensuring that critical cases are addressed promptly. It can also quickly review policy details and determine coverage for a claim to streamline the initial assessment process.

Smarter, Faster Claims

That sensor that detected a water leak in the upstairs bathroom? The AI driving that experience automates first notice of loss (FNOL) and proactively asks the policyholder if they’d like to submit a claim. And it’s handling a rising share of processes beyond that point. In fact, McKinsey projects that by 2030, as much as half of all routine claims may be resolved digitally.

The same smartphone apps used to document and assign values to property assets can also be used to assess the damage done to them by fire, flood, tornados, and more. Solutions like PLNAR use AI and augmented reality to scan home interiors and reconstruct them in an ad hoc digital twin that places adjusters directly into the space, complete with accurate measurements and the estimated cost of repair.

The Rewards of Loyalty

This means AI is able to automate the vast majority of low-severity property claims, while routing those that require expert judgment and empathy to human beings. Over time, AI is likely to harness the same data sources used to understand and price risk to verify more complex claims. Geospatial analytics-based property condition intelligence, for instance, can validate storm damage to roofs, or assess damage after a large-scale catastrophe.

This is about more than just cost-savings. It’s also a long-term revenue generator. That’s because studies have shown that more than 86% of policyholders with a positive claims experience say they will “definitely” renew their policies, while 45% of less satisfied claimants are at risk of switching carriers.

According to McKinsey, customer experience leaders in the P&C sector outperform peers in total shareholder returns by 65% and demonstrate higher EBIT growth by 4%. Assuming average EBIT is 10-15%, that’s a 25% to 40% relative improvement in profitability. To that end, JD Powers’ 2025 Property Claims Satisfaction Survey points out that insurers offering AI-enabled digital claims reporting and support channels that facilitate proactive updates and support see satisfaction scores that are nearly twice as high as those without them.

Fraud: More Than Meets AI

According to Deloitte, AI technologies for detecting and preventing fraud could help P&C insurers save as much as $80 billion to $160 billion a year by 2032. That could make a big difference at a time when fraud losses now top $122 billion annually—resulting in the average American family paying an extra $400 to $700 in premiums each year.

An accurate, up-to-date understanding of property condition, for instance, can be useful in countering the kind of fraudulent claims and “free roof” scams afflicting insurers in Florida and elsewhere these days. Among other things, it can easily identify instances when a roof was not replaced after a claim. As Risk & Insurance points out, the most frequently-updated varieties can also help verify damage extent and location not visible during physical inspections—reducing injury risk to inspectors in the aftermath of large-scale catastrophes.

This is especially important given the rising use of images or videos that have been doctored or scraped off the Internet as part of claims scams—including deep fakes, which use AI to fool human beings.

Today, there are a number of apps that can be exploited for claims that never occurred, or to document valuation of assets that don’t even exist. According to a recent Capgemini report, 62% of insurers stated they believe AI and machine learning can reduce fraud losses and flag inconsistencies that human reviewers might miss. the case of deep fakes, AI will need to be leveraged to fight AI with solutions such as Attestiv, which uses machine learning and other technologies to authenticate digital media from any person or device—including deep fakes.

This Is All Just the Beginning

New sources of data, and the ability to apply it through AI, will increasingly become a significant differentiating source of insight and value for property insurers. It’s this ability to launch new products and services that make the world more insurable, accelerate claims in ways the benefit insured at what can be a time of high stress, and improve fraud management in ways that lower the cost burden on homeowners.

In some ways, the AI revolution in property insurance puts new urgency attracting talent and the ability to leverage external, cloud-connected solutions instead of relying solely on internal development resources. In the $1.05 trillion P&C insurance market, the one who best harnesses the power of AI is very likely to come out ahead.

To learn how AI-based property condition intelligence can help insurers select better risks, reduce expenses, and improve customer experience, visit our Geospatial Analytics page.