2024 Wildfire Season Outlook: 3 Top Lessons from 2023

As the 2024 wildfire season gets underway, property insurers would be wise to sift through lessons to be learned from the 2023 season and the catastrophes in Lahaina and Yellowknife.

Last August, devastating wildfires killed as many as 115 people and gutted more than 2,200 homes and businesses in Maui, Hawaii—while an inferno sent more than 20,000 residents from the capital of Canada’s Northwest Territories fleeing from their homes. In the months since, P&C insurers have continued to grapple with ways to improve risk modeling amid the new realities of wildfire risk.

It’s easy to see why. After 2022’s relative calm and a welcome return of heavy precipitation in much of the Western United States last winter, modeling from many property risk data providers predicted another reprieve from recent wildfire trends. But the respite was short-lived: A protracted heatwave resulted in the hottest June in 174 years—and a jump in wildfire activity that put US totals at nearly 80% of the 10-year average, with 56,580 wildfires.

North of the US border in Yellowknife, record temperatures and dry conditions contributed to the more than 45 million acres burned across Canada last summer—in a nation that normally sees just six million acres burn yearly. In Lahaina, the wildfires were fanned by, of all things, the winds of a hurricane hundreds of miles away. As Lt. Gov. Sylvia Luke told the Wall Street Journal, “We never expected a hurricane, which did not touch down on our land, would cause these kinds of wildfires.”

The result was the deadliest US wildfire in 100 years. According to Hawaii’s state insurance division, more than 3,700 homeowners and businesses have filed insurance claims, with nearly 1,500 properties suffering a total loss. By this May, the tally for insured losses topped $3 billion across 200 insurers.

Unfortunately, Maui’s far from alone. In California, residents and businesses have endured two roughly $10 billion-insured-loss wildfires every year since 2017. This year, expectations were for a slow-start to a season and hopes for “below average” risk levels in much of the American West. But by mid-June, the optimism grew more muted with a number of wildfires erupting in the central valley and southern regions of California. If that sounds familiar, the 2023 wildfire season offers four critical insights for residential and commercial property underwriters.

#1 Wildfire Season Is Now More ‘On’ Than ‘Off’

Lahaina and Yellowknife were a sign of things to come. Persistent drought conditions and the compounding effects of climate change have put 44.1 million homes in booming Wildland Urban Interfaces, including 5.1 million in California and 3.2 million in Texas, more vulnerable to wildfires.

One quantified example comes in the form of a recent study of hourly observation data from 476 weather stations across the lower 48 states over the last 51 years. According to the findings, the average annual number of weather days conducive to wildfires is increasing throughout the majority of California, with jumps as high as 61 additional “fire weather” days per year since 1973. Over the past 50 years, wildfire season in the western US has grown from 5 months per year to over 7 months.

As the Washington Post reports, this dynamic is also driving fire eastward across the United States. As well as driving them north. By 2035, Oregon and Washington are likely to see double the amount of wildfires seen in 1993. Across the Western US, there was a 172% increase in burned areas between 1971 and 2021, according to Drought.gov. In coming years, additional increases could top 52%—and the worse it gets, the worse it will get. As the planet continues to warm, carbon emissions from fossil fuels will continue to dry out wilderness areas everywhere, making them more prone to wildfire, creating a catastrophic feedback loop: Wildfires worsened by climate change will, in turn, worsen climate change.

As David Sampson, president of the American Property Casualty Association and a member of President Biden’s Wildland Fire Mitigation and Management Commission puts it, “There is no wildfire season anymore—it’s year round.”

As the ferocity, frequency, and footprint of wildfire risk continues to expand, many insurers have been under pressure to add exclusions, increase premiums, or pull back on issuing new policies in California and elsewhere. But that may not be a viable growth strategy long term—nor is it even necessary. Today, technologies exist to help insurers revolutionize how they write, mitigate, and respond to wildfire risk.

#2 The Right Data Trumps the Unexpected

The industry’s technological revolution, particularly the rise of next-generation data ecosystems, is laying the foundation for a new, transformative era of property risk data and analytics. The problem for most insurers is that their traditional sources of property data, territory-based risk models, and past loss experience are based on 50-year-old assumptions. And when your data is inaccurate or outdated, the investment and faith you put into risk models and analytics go to waste. Unfortunately, most carriers don’t even realize much better options are available.

Instead of relying solely on outdated data sources, these assets must be augmented with continuously updated property intelligence that provides a holistic view of wildfire risk at the individual property level. Not just today, but as that risk—and its compounding financial impact—evolves over time.

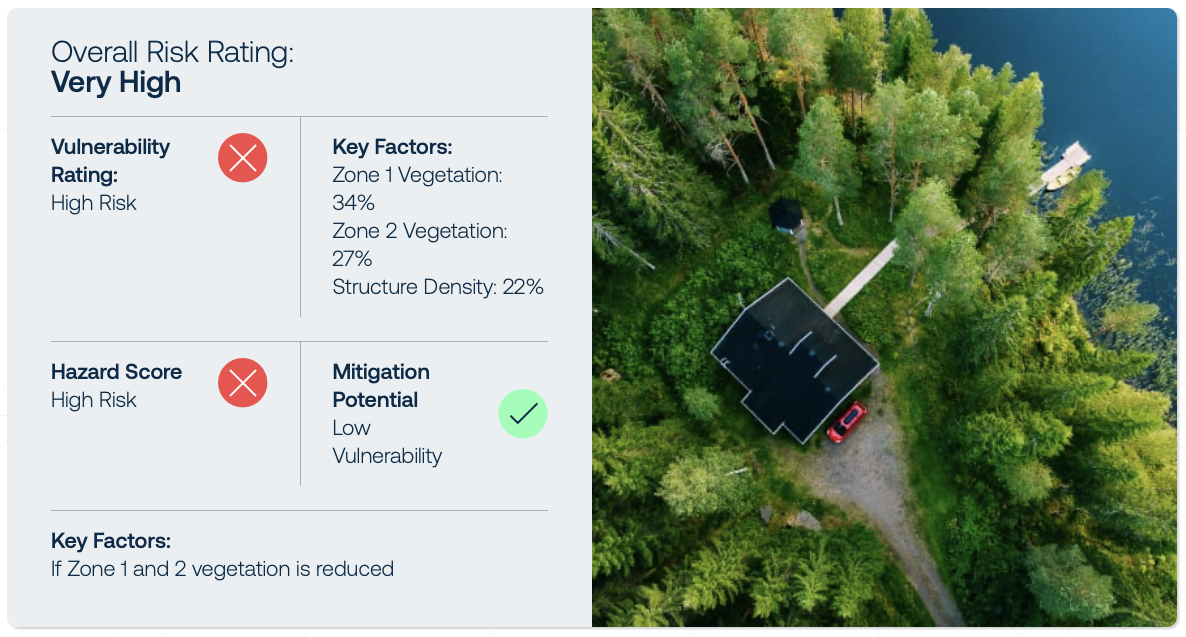

CAPE Wildfire Intelligence combines the highest-resolution, multi-source imagery, geospatial AI, and dozens of wildfire-relevant data points to give insurers a high-fidelity understanding of residential and commercial wildfire risk with surgical precision. This includes a suite of wildfire risk rates or standalone, loss-predictive attributes such as wildland fuel load, roof material, building density, presence of a wood deck, Katabatic wind zones, drought levels, and more for any of more than 120 million properties in the US.

Insurers leveraging this kind of data are starting to gain an advantage. According to McKinsey, a key commonality among today’s most competitive insurers is the strategic application of high-quality external data sources combined with advanced analytics capabilities. Across the board, these investments have been shown to help insurers improve loss ratios by up to 5%, increase new premiums by up to 15%, and improve retention of profitable segments by up to 10%.

In California, an $11 billion insurance market, instead of reducing exposure to wildfire risk or leaving the market altogether, carriers can now identify the 10% of the state that accounts for 90% of the potential property damage. Winners there could see any of the measures above skyrocket. As McKinsey puts it, “external data is the fuel that can ignite the value of analytics.”

With instant, on-demand access to wildfire vulnerability and risk metrics, insurers can more effectively make their case to regulators on pricing—and can more accurately price policies to reflect actual risk. Indeed, carriers like Hippo are equipping themselves with this kind of insight in order to underwrite and price property coverage where less-competitive rivals fear to tread. Instead of bypassing entire neighborhoods or abandoning entire markets, insurers can spur growth by pricing risk accurately while avoiding bad bets.

#3 Prevention Now Can Pay Off Later

With the price of construction materials up 33.9% and contractor services up 27% since 2020—and with the global protection gap hitting 69% in the past year—an opportunity exists for carriers to reward homeowners and businesses to mitigate wildfire risk. In California, it’s now required under the state’s Safer from Wildfires framework, which went into effect last year. While it’s still unclear how effective this first-of-its-kind regulation has been, it may presage a wave of similar mandates elsewhere.

What is undeniable, however, is that mitigation efforts can pay off for the insured and insurer alike. According to Moody’s, clearing vegetation from around a dwelling combined with structure improvements can reduce wildfire risk up to 75%. Here too, insurers harnessing continuously-updated wildfire intelligence that leverages high-resolution aerial imagery, computer vision, and AI technologies will have a distinct advantage over those requiring on-site inspections.

Returning to CAPE’s solution once more, our transparent analytics inform insurers and homeowners of the contributing factors to a property’s wildfire risk, actions that can be taken to mitigate that risk, and the quantified impact such actions will have on both risk and rate.

According to a subsequent 2023 study from Moody’s, Southern California Edison’s steps to harden its power grid has reduced the risk of catastrophic wildfire losses by up to 80%. The untapped market for risk prevention services could be enormous. Nationwide, only 4.3% of consumers used risk-prevention services offered by insurers in 2023—suggesting extremely low awareness and significant upside potential.

Learning From 2023 & Lahaina

Then again, that lack of consumer awareness for risk-mitigation services may stem from another dynamic. According to Capgemini, only 35% of carriers have adopted the kinds of technologies described in this post. As the threat posed by wildfires and other natural catastrophes continues to grow, those that do will differentiate themselves from what, in some places, is a dwindling pack. Others behind the curve might want to take steps to catch up—for their own bottom lines and those of their customers.

As recently as January, for instance, nearly half the pre-fire population of Lahaina were still seeking a place to live. “I want to start living life instead of being in constant survival mode,” resident Amy Chadwick told the Washington Post, adding that she is moving to the mainland with her husband, mother, and two kids. “We have to leave our island home. It’s heartbreaking.” With the right data, such upheaval (and its associated losses) may be avoidable.

To learn more about CAPE Wildfire Intelligence, click here.